Superior Courts Act, 2013

Superior Courts Act, 2013

R 385

Banks Act, 1990 (Act No. 94 of 1990)RegulationsRegulations relating to BanksChapter II : Financial, Risk-based and other related Returns and Instructions, Directives and Interpretations relating to the completion thereof23. Credit risk: monthly returnDirectives and interpretations for completion of monthly return concerning credit risk (Form BA 200)Subregulation (6) Method 1: Calculation of credit risk exposure in terms of the simplified standardised approach |

| (6) | Method 1: Calculation of credit risk exposure in terms of the simplified standardised approach |

Unless specifically otherwise provided in these Regulations, a bank that adopted the simplified standardised approach for the measurement of the bank's exposure to credit risk arising from positions held in its banking book shall risk weight its relevant exposure, net of any credit impairment, in accordance with the relevant requirements specified below:

| (a) | In the case of exposure to sovereigns, central banks, public-sector entities, banks, securities firms and corporate institutions, in accordance with the provisions of table 1 below: |

|

Table 1 |

|||||||||||||||

|

Claim in respect of— |

Export Credit Agencies: risk scores relating to sovereign1 |

||||||||||||||

|

0-1 |

2 |

3 |

4 to 6 |

7 |

|||||||||||

|

Sovereigns (including the Central Bank of that country) |

0% |

20% |

50% |

100% |

150% |

||||||||||

|

Public sector entities |

20% |

50% |

100% |

100% |

150% |

||||||||||

|

Banks 2, 3, 4 |

20% |

50% |

100% |

100% |

150% |

||||||||||

|

Securities firms 2, 4, 6 |

20% |

50% |

100% |

100% |

150% |

||||||||||

|

Banks: short-term claims 5 |

20% |

20% |

20% |

50% |

150% |

||||||||||

|

Securities firms: short-term claims 5, 6 |

20% |

20% |

20% |

50% |

150% |

||||||||||

|

Corporate entities |

Any corporate exposure, including claims on insurance companies |

||||||||||||||

|

100% |

|||||||||||||||

|

|||||||||||||||

|

|||||||||||||||

[Regulation 23(6)(a) substituted by section 2(d) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

| (b) | Subject to the provisions of subparagraph (v) below, in the case of an exposure that meets all the respective requirements and criteria specified in subparagraphs (i) to (iv) below, which exposure shall be regarded as forming part of the bank’s retail portfolio, excluding any exposure that is overdue, at a risk weight of 75 per cent. |

| (i) | Criteria relating to orientation |

The exposure shall relate to—

| (A) | an individual person or persons; or |

| (B) | a small or medium sized entity or business, as envisaged in subparagraph (v)(A) below. |

| (ii) | Criteria relating to the product |

The exposure shall be in the form of—

| (A) | a revolving credit exposure or line of credit, including exposures relating to credit cards and overdraft facilities; |

| (B) | a personal term loan or lease, including instalment loans, vehicle finance and leases, student and educational loans and personal finance; or |

| (C) | a small business facility or commitment, as envisaged in subparagraph (v)(A) below, |

provided that the exposures specified below shall at no stage form part of a bank’s retail portfolio envisaged in this paragraph (b).

| (i) | Securities such as bonds and equities, whether listed or unlisted; |

| (ii) | Any derivative instrument or exposure; and |

| (iii) | Residential mortgage loans that qualify for inclusion in the category of claims secured by residential property. |

| (iii) | Criteria relating to granularity |

In order to ensure that the retail portfolio of the reporting bank is sufficiently diversified, no aggregated exposure to a counterparty shall exceed 0.2% of the aggregate amount relating to the bank’s retail portfolio.

For the purposes of this subparagraph (iii)—

| (A) | aggregated exposure means the relevant gross amount of all forms of debt included in the retail portfolio before any form of credit risk mitigation has been taken into consideration; |

| (B) | the bank shall calculate the relevant gross amount after applying all relevant credit conversion factors related to off-balance sheet items; |

| (C) | counterparty means one or more persons or entities that may be considered a single beneficiary, including small businesses affiliated to one another; and (D) all retail exposures that are overdue as envisaged in paragraph (e) below shall be excluded from the aggregate amount when the bank calculates the said granularity of the retail portfolio. |

| (iv) | Low value of individual exposures |

An exposure to an individual person or small business shall be included in the retail portfolio only when the aggregate amount of the said exposure after the application of the relevant credit conversion factors but before the effect of any risk mitigation is taken into consideration, is less than or equal to such an amount as may be specified in writing by the Authority from time to time.

| (v) | When the exposure— |

| (A) | relates to an entity, institution or person with an outstanding exposure of less than or equal to such amount as may be directed in writing by the Authority, and complies with such further conditions as may be directed in writing by the Authority, the bank’s exposure to that entity, institution or person shall be regarded as a retail small and medium entity (SME) exposure to which the bank shall assign a risk weight of 75 per cent; |

| (B) | arises from obligors who qualify as transactors, that is, when any outstanding balance has been repaid in full at each relevant scheduled repayment date for the previous 12 months in relation to a facility such as a credit card facility, or when no drawdowns have been made over the previous 12 months in respect of an overdraft facility, such retail exposures may be risk-weighted at 45%; |

| (C) | relates to lending secured by mortgage on an occupied urban residential dwelling or occupied individual sectional title dwelling or similar exposure to residential real estate, the bank shall treat that exposure in accordance with the relevant requirements specified in paragraph (c) below; |

| (D) | is unhedged from a borrower’s currency risk perspective, that is, the borrower has no natural or financial hedge against the exposure to foreign exchange risk arising from any currency mismatch between the currency of the borrower’s source(s) of income and the currency of the loan, the bank shall multiply the risk weight specified in this paragraph (b) with 1.5, provided that for purposes of this paragraph (b)— |

| (i) | a natural hedge means the borrower, in its normal operating procedures, receives income in foreign currency, such as, for example, in the form of remittances, rental income or salaries, that matches the currency of the relevant loan; |

| (ii) | a financial hedge includes a legal contract, such as, for example, a forward contract, with a financial institution; |

| (iii) | and the application of the multiplier, natural or financial hedge shall be considered sufficient only when it covers at least 90% of the relevant loan instalment, regardless of the number of hedges. |

| (E) | does not comply with all the requirements specified in this paragraph (b), the bank shall risk weight that exposure at no less than 100 per cent, in accordance with the relevant requirements specified in paragraph (j) below. |

[Regulation 23(6)(b) substituted by section 2(e) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

| (c) | Subject to the provisions of subparagraph (xiv) below, in the case of lending secured by mortgage on an occupied urban residential dwelling or occupied individual sectional title dwelling or similar exposure to residential real estate, that is, an exposure secured by immovable property that has the nature of a dwelling and complies with all the respective requirements specified in relevant laws and regulations that enable the property to be occupied by the owner, or by another person with the consent of the owner, as a primary residence for residential housing purposes, when the exposure is not in default, and to the extent that the exposure complies with all the respective requirements and criteria respectively specified in subparagraphs (i) to (x) below, in accordance with the respective requirements specified in table 1 below, provided that when the relevant exposure does not comply with the requirements respectively specified in subparagraphs (i) to (x), the bank shall apply to that residential real estate exposure the relevant requirements specified in subparagraphs (xi) to (xiii) below. |

|

Table 1 |

||||||||||

|

Exposure amount 1; 2 |

||||||||||

|

Loan to Value (LTV) |

LTV ≤ 50% |

50% < LTV ≤ 60% |

60% < LTV ≤ 80% |

80% < LTV ≤ 90% |

90% < LTV ≤ 100% |

LTV > 100% |

||||

|

Risk weight |

20% |

25% |

30% |

40% |

50% |

70% |

||||

|

||||||||||

| (i) | Underwriting policies, processes, standards and procedures |

As a minimum, the bank shall have in place robust underwriting policies, processes, standards and procedures with respect to the granting of residential real estate exposure, mortgage loans or similar exposures to residential property—

| (A) | that include and define appropriate metrices, such as, for example— |

| (i) | the loan’s debt service coverage ratio, to prevent over-indebtedness of the borrower, and specify all relevant or material required information in respect of the said metric; |

| (ii) | appropriate loan-to-value (LTV) ratios; |

| (B) | that include, among others— |

| (i) | an assessment of the ability of the borrower to repay the loan, provided that when the prospect for servicing the relevant loan depends materially on the cash flows generated by the property securing the loan, rather than on the underlying capacity of the borrower to service the debt from other sources, and provided that the requirements specified in subparagraphs (xii) or (xiii) do not apply, the bank shall risk weight the relevant exposure in accordance with the requirements specified in subparagraph (xi) below; |

| (ii) | effective procedures to verify the relevant required information related to income, and any other relevant financial information; |

| (C) | that ensure, among others- |

| (i) | effective collateral management; |

| (ii) | the prudent use of mortgage insurance; |

| (iii) | that mortgage insurance in no case serves as a substitute for sound underwriting practices applied by the bank; |

| (iv) | that the bank’s underwriting policies are sufficiently robust and remain appropriate when the repayment of the mortgage loan depends materially on the cash flows generated by the property, including relevant metrices, such as, for example, an occupancy rate of the property; |

| (ii) | Finished property |

The property securing the exposure shall be fully completed, provided that, subject to such additional requirements as may be specified in writing by the Authority, a bank may apply the risk weights specified in this paragraph (c) in respect of an exposure secured by residential property under construction or land upon which residential property would be constructed when the exposure relates to an individual.

| (iii) | Legal enforceability |

The relevant collateral agreement and any potential claim on the property shall be legally enforceable in all relevant jurisdictions, and the legal process underpinning the collateral agreement shall enable the bank to realise the value of the property serving as collateral within a reasonable period of time.

| (iv) | Claims over the property |

In respect of lending to the borrower, secured by mortgage, the bank shall hold a first lien mortgage or similar legally enforceable claim over the property, or the first lien or claim and any sequentially lower ranking lien(s) or claim(s). In other words, there shall be no lien or claim with a ranking higher than the bank’s claim against the relevant residential property, from any other bank or lender, provided that—

| (A) | in exceptional cases, subject to such further conditions as may be specified in writing by the Authority, when a subsequent junior lien or claim provides the bank with a claim for collateral that is legally enforceable and constitutes an effective credit risk mitigant, the relevant exposure related to that junior lien or claim held by another bank may also be risk weighted in accordance with the relevant requirements specified in this paragraph (c); |

| (B) | in all relevant cases, the bank shall ensure that any relevant framework governing liens or claims over or encumbrance of the relevant property provides the bank holding the lien on or claim against the property, the right to initiate the sale of the property, independently from any other entity that may hold a lien on or claim over the property; and |

| (C) | where the subsequent sale of the relevant property is not carried out by means of a public auction, the bank holding the senior lien or claim shall take all necessary and reasonable steps to obtain a fair market value or the best price that may reasonably be expected to be obtained in the circumstances when exercising its power of sale, that is, the bank holding the senior lien or claim to sell the property on its own shall not sell the relevant property at an unreasonable discounted value to the detriment of any person either holding a junior lien over the property or otherwise having a legal right in respect of that property; |

| (v) | Prudent valuation of property |

The bank shall ensure that all relevant loan-to-value (LTV) ratios, that is, the amount of the loan divided by the value of the property multiplied by one hundred, are calculated in a prudent manner, in accordance with the respective requirements specified below:

| (A) | The outstanding amount of the mortgage loan shall include any undrawn committed amount related to the loan, provided that— |

| (i) | when the bank granted different loans secured by the same property and the respective loans are sequential in ranking order, that is, there is no intermediate lien from any other bank, the bank shall add together and risk-weight the respective components of the loan as a single exposure, when calculating the relevant required LTV ratio; |

| (ii) | when the Authority approved in writing that a junior lien or claim held by a bank other than the bank holding the senior lien may also be risk weighted in accordance with the relevant requirements specified in this paragraph (c), the bank with the junior lien shall include in the relevant loan amount all other loans secured with liens of equal or higher ranking than the bank’s lien or claim securing the loan for purposes of determining the relevant LTV bucket and the related risk weight for the junior lien. |

When the bank has insufficient information for ascertaining the ranking of any other liens or claims held by any other person, the bank shall assume that those liens or claims rank senior to or pari passu with the junior lien or claim held by the bank.

| (iii) | the bank shall calculate the relevant loan amount gross of any relevant credit impairment or provision and any relevant credit risk mitigation, unless the bank holds deposits that meet all the respective requirements specified in these Regulations for set-off or on-balance sheet netting, which deposits have been pledged unconditionally and irrevocably for the sole purpose of reducing the outstanding balance of the relevant mortgage loan; |

| (B) | Unless directed otherwise in writing by the Authority, the bank shall maintain the value of the property as at the date of the relevant loan origination, provided that— |

| (i) | the bank shall adjust the aforesaid value downwards when an extraordinary, idiosyncratic event occurs, resulting in a probable permanent reduction in the value of the property; |

| (ii) | when the bank previously adjusted the property’s value downwards, as envisaged in sub-item (i) hereinbefore, the bank may subsequently make an upward adjustment to the value of the property, but in no case to a value higher than the value of the property at origination; |

| (iii) | the bank may take into consideration modifications made to the property after the date of origination of the loan that unequivocally increase the property’s value; |

| (C) | The value of the relevant property— |

| (i) | shall be determined independently from the bank’s mortgage acquisition, loan processing and loan decision process; |

| (ii) | shall exclude any expectation related to price increases; |

| (iii) | shall be market related; |

| (D) | When a mortgage loan is financing the purchase of the relevant property, the value of the property for LTV purposes shall not be higher than the effective purchase price. |

| (E) | The value of the property shall not depend materially on the performance of the borrower. |

| (vi) | Documentation |

The bank shall ensure that all the relevant information required at loan origination and for monitoring purposes is duly documented, including, as a minimum, all relevant required information related to—

(A) the ability of the borrower to repay the loan; and

(B) the valuation of the relevant property.

| (vii) | Credit risk mitigation in relation to LTV |

The bank shall determine the appropriate LTV bucket and the related risk weight envisaged in this paragraph (c), prior to taking any credit risk mitigation into account, although the bank may thereafter take into consideration a guarantee, financial collateral or mortgage insurance that complies with the respective requirements related to eligible risk mitigation in relation to the bank’s exposures secured by residential real estate when the bank eventually determines the relevant required amount of capital and reserve funds to be maintained by the bank.

| (viii) | Occupied |

For purposes of this paragraph (c), only urban residential dwellings or individual sectional title dwellings that are occupied or intended to be occupied as the principal place of residence of either the borrower or, with the consent of the borrower, a person other than the borrower, shall be regarded as adhering to the requirement of being “occupied”.

In this regard, although the intention of the borrower may be an important indicator, the purpose for which the dwelling is/will be utilised shall be determined with reference to objective factors and reasonability.

For example, the fact that the residence may be unoccupied for short periods of time, such as when the resident is on vacation, does not change the classification. On the other hand, a residence used mainly for purposes of vacation or to conduct business activities can clearly not be regarded as the principal place of residence.

| (ix) | Urban |

For the purposes of this paragraph (c), urban area means an area inside the boundaries of any local government area fixed by law.

| (x) | Dwelling |

For the purposes of this paragraph (c), dwelling means any building that—

| (A) | after its construction contains or will contain living rooms with a kitchen and the usual appurtenances and permanent provision for lighting, water supply, drainage and sewerage, whether such building is or is to be constructed as a detached or semi-detached building or is or is to be contained in a block of buildings; |

| (B) | is designed and utilised or meant to be utilised for residential purposes; and |

| (C) | is located in an area— |

| (i) | in which the majority of the premises are residential premises; or |

| (ii) | comprising at least 100 residential premises and which is defined for this purpose by means of cadastral boundaries, as shown on the compilation maps of the Surveyor General. |

| (xi) | When the requirements specified in subparagraphs (i) to (x) hereinbefore are met, but the repayment of the loan or the prospect for recovery in the event of default depends materially on the cash flows generated by the relevant residential property securing the residential exposure, such as, for example, the cash flows generated by lease or rental payments, or the sale of the residential property, rather than on the underlying capacity of the borrower to repay the debt from other sources, the bank shall also have in place appropriately conservative matrices, such as, for example, a minimum occupancy rate in relation to the property. The bank shall in such cases risk weight that residential real estate exposure in accordance with the requirements specified in table 2 below, instead of table 1 hereinbefore: |

|

Table 1 |

||||||||||

|

Exposure amount 1; 2 |

||||||||||

|

Loan to Value (LTV) |

LTV ≤ 50% |

50% < LTV ≤ 60% |

60% < LTV ≤ 80% |

80% < LTV ≤ 90% |

90% < LTV ≤ 100% |

LTV > 100% |

||||

|

Risk weight |

30% |

35% |

45% |

60% |

75% |

105% |

||||

|

||||||||||

| (xii) | In the case of exposure related to land acquisition, development and construction of residential real estate, the bank may risk weight those exposures at 100 per cent when the following criteria are met: |

| (A) | the bank has in place robust and prudent underwriting standards that comply with the relevant requirements specified in subparagraph (i) hereinbefore; and |

| (B) | written pre-sale or pre-lease contracts that are legally enforceable and that amount to a significant portion of total contracts are in place, and the relevant purchaser/renter has made a substantial cash deposit that is subject to forfeiture if the contract is terminated, or has substantial equity at risk, that is, borrower-contributed equity to the real estate’s appraised as-completed value, is in place. |

Provided that—

| (i) | for purposes of this subregulation (6)(c), exposure related to land acquisition, development and construction of residential real estate— |

| (aa) | means loans to companies or special-purpose vehicles (SPVs) financing any land acquisition for development and construction purposes, or development and construction of any relevant residential property; |

| (bb) | does not include the acquisition of forest or agricultural land, where there is no planning consent or intention to apply for planning consent; and |

| (ii) | any relevant exposure related to land acquisition, development and construction of residential real estate that does not comply with the criteria specified hereinbefore shall be risk-weighted at 150 per cent; |

| (xiii) | When the aforementioned residential real estate exposure is unhedged from a borrower’s currency risk perspective, that is, the borrower has no natural or financial hedge against the exposure to foreign exchange risk arising from a mismatch between the currency of the borrower’s source(s) of income and the currency of the loan, the bank shall multiply the relevant risk weight specified in this paragraph (c) with 1.5, subject to a maximum risk weight of 150%, provided that for purposes of this paragraph (c)— |

| (A) | a natural hedge means the borrower, in its normal operating procedures, receives income in foreign currency, such as, for example, in the form of remittances, rental income or salaries, that matches the currency of the relevant loan; |

| (B) | a financial hedge includes a legal contract, such as, for example, a forward contract, with a financial institution; |

| (C) | and the application of the multiplier, natural or financial hedges envisaged in items (A) and (B) respectively shall be considered sufficient only when they cover at least 90% of the relevant loan instalment, regardless of the number of hedges. |

| (xiv) | When a bank does not comply with all the respective requirements specified in subparagraphs (i) to (x) hereinbefore, and, in addition, the relevant residential real estate exposure does not fall within the ambit of any of the exposure types envisaged in subparagraphs (xi) to (xiii), the bank may risk weight the relevant residential real estate exposure based upon the risk weight of an unsecured exposure to the relevant counterparty. For example, in the case of an exposure to an individual, the bank may apply a risk weight of 75 per cent, provided that when the Authority, in its sole discretion, determines that the risk weight of 75 per cent underestimates the bank’s actual exposure to risk and is too low for specified types of residential real estate exposure which does not comply with all the respective requirements specified in subparagraphs (i) to (x) of this paragraph (c), the Authority may direct the bank in writing to risk weight the relevant residential real estate exposure at 150 per cent. |

[Regulation 23(6)(c) substituted by section 2(f) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

| (d) | In the case of lending secured by mortgage on commercial real estate, including any exposure secured by immovable property other than exposure qualifying for inclusion in paragraph (c) as a residential real estate exposure, and to the extent that the bank complies with the respective requirements specified in paragraphs (c)(i) to (c)(vii), insofar as they are relevant, the bank shall risk weight that relevant exposure in accordance with the respective requirements specified in table 1 below. Provided that when the exposure does not comply with the relevant requirements specified in paragraphs (c)(i) to (c)(vii) hereinbefore or the repayment of the loan depends materially on the cash flows generated by the relevant commercial real estate securing the loan, the bank shall apply to that commercial real estate exposure the relevant requirements and risk weights specified in subparagraphs (i) to (iii) below. |

|

Table 1 |

||

|

Loan to Value (LTV) |

LTV ≤ 60% |

LTV > 60% |

|

Risk weight |

Min (60%, RW of counterparty) |

RW of counterparty |

| (i) | When the relevant requirements specified in paragraphs (c)(i) to (c)(vii) hereinbefore are met, insofar as they are relevant, except that the repayment of the loan or the prospects for recovery in the event of default depends materially on the cash flows generated by the relevant commercial real estate securing the exposure, such as, for example, the cash flows generated by lease or rental payments, or the sale of the commercial real estate or property, rather than on the underlying capacity of the borrower to repay the debt from other sources, the bank shall risk weight that relevant commercial real estate exposure in accordance with the requirements specified in table 2 below: |

|

Table 2 |

|||

|

Loan to Value (LTV) |

LTV ≤ 60% |

60% < LTV ≤ 80% |

LTV > 80% |

|

Risk weight |

70% |

90% |

110% |

| (ii) | In the case of exposure related to land acquisition, development and construction, other than for residential real estate purposes envisaged in paragraph (c)(xii), the bank shall risk weight the relevant exposure at 150% provided that for purposes of this subregulation (6)(d), exposure related to land acquisition, development and construction of commercial property— |

| (aa) | means loans to companies or special-purpose vehicles (SPVs) financing any land acquisition for development and construction purposes, or development and construction of any relevant commercial property; |

| (bb) | does not include the acquisition of forest or agricultural land, where there is no planning consent or intention to apply for planning consent; |

| (iii) | When a bank does not comply with all the respective requirements specified in paragraphs (c)(i) to (c)(vii), insofar as they are relevant, and, in addition, the relevant commercial real estate exposure does not fall within the ambit of exposure envisaged in subparagraphs (i) and (ii) hereinbefore and does not materially dependent on the cash flows generated by the property, the bank may risk weight the relevant commercial real estate exposure based upon the risk weight of an unsecured exposure to the relevant counterparty. For example, in the case of an exposure to an SME, the bank may apply a risk weight of 85 per cent, provided that when the Authority, in its sole discretion, determines that the risk weight of the relevant counterparty underestimates the bank’s actual exposure to risk and is too low for specified types of commercial real estate exposure which does not comply with all the respective requirements specified in paragraphs (c)(i) to (c)(vii), the Authority may direct the bank in writing to risk weight the relevant commercial real estate exposure at 150 per cent; |

[Regulation 23(6)(d) substituted by section 2(g) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

| (e) | In the case of an exposure, other than an exposure secured by residential real estate or mortgage on residential property as envisaged in paragraph (c), which exposure is in default— |

| (i) | the bank shall risk weight the unsecured portion of the exposure, net of any relevant specific impairment, provision for loss or partial write-off, as follows: |

| (A) | 150 per cent when the specific credit impairment in respect of the outstanding amount of the exposure is less than 20 per cent; |

| (B) | 100 per cent when the specific credit impairment in respect of the outstanding amount of the exposure is equal to or more than 20 per cent; |

| (C) | 50 per cent when the specific credit impairment in respect of the outstanding amount of the exposure is equal to or more than 50 per cent, |

Provided that, in the case of retail exposures, the bank may apply the criteria related to default at the level of a particular credit obligation, instead of at the level of the relevant person or borrower, that is, a default by a borrower on one obligation does not necessarily mean that the bank has to treat all other relevant obligations of that person or borrower towards the bank or banking group of which the bank is a member, as being in default;

[Regulation 23(6)(e) substituted by section 2(h) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

| (f) | In the case of an exposure secured by residential real estate or mortgage on an occupied urban residential dwelling or occupied individual sectional title dwelling as envisaged in paragraph (c), which exposure is in default, the bank shall risk weight the exposure net of any relevant specific impairment, provision for loss or partial write-off at 100 per cent when the repayment of the loan does not materially depend on the cash flows generated by the property securing the exposure, provided that— |

| (i) | the bank may take any relevant eligible risk mitigation into consideration in accordance with the relevant requirements specified in these Regulations; |

| (ii) | in the case of residential real estate exposures, the bank may apply the criteria related to default at the level of a particular credit obligation, instead of at the level of the relevant person or borrower, that is, a default by a borrower on one obligation does not necessarily mean that the bank has to treat all other relevant obligations of that person or borrower towards the bank or banking group of which the bank is a member, as being in default. |

[Regulation 23(6)(f) substituted by section 2(i) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

| (g) | In the case of any off-balance-sheet item or exposure, other than— |

| (i) | a securities financing transaction that exposes the bank to counterparty credit risk, in respect of which the relevant credit equivalent amount shall be calculated in accordance with the relevant requirements related to— |

| (A) | the internal model method set out in subregulation (19) when the bank obtained the required prior written approval of the Authority; or |

| (B) | in all other relevant cases, the comprehensive approach set out in subregulation (9)(b); |

| (ii) | a derivative contract that exposes the bank to counterparty credit risk, in respect of which the relevant credit equivalent amount— |

| (A) | shall be calculated in accordance with the relevant requirements related to the internal model method set out in subregulation (19) when the bank obtained the required prior written approval of the Authority; or |

| (B) | shall in all other relevant cases be calculated in accordance with the requirements specified in subregulations (15) to (19); |

| (iii) | posted collateral that is subject to the requirements specified in subregulation (18) relating to the standardised approach for counterparty credit risk or in subregulation (19) relating to the internal model method for counterparty credit risk; |

| (iv) | unsettled transactions or failed trades related to securities, commodities or foreign exchange, as envisaged in subregulation (20), the relevant exposure and related required amount of capital and reserve funds which shall be calculated in accordance with the relevant requirements specified in subregulation (20); or |

| (v) | securitisation or resecuritisation exposure as envisaged in paragraph (h) below, |

the bank shall convert the off-balance-sheet item or exposure into a credit exposure equivalent amount by multiplying the relevant item or exposure with the relevant credit-conversion factor specified in table 1 below:

|

Table |

|||||||||||||||||||||

|

Description |

Credit conversion factor |

||||||||||||||||||||

|

Any solicitation limit, that is, a facility not yet contracted |

0 per cent |

||||||||||||||||||||

|

Such arrangements regarded by the Authority as not falling within the ambit of commitments as envisaged in these Regulations and that comply with specified requirements 1 |

0 per cent |

||||||||||||||||||||

|

Any revocable commitment2 unconditionally cancellable at any time by the bank without prior notice or that effectively provide for automatic cancellation due to deterioration in the relevant borrower’s creditworthiness |

10 per cent |

||||||||||||||||||||

|

Self-liquidating trade letters of credit with an original maturity of less than one year arising from the movement of goods, such as, for example, documentary credits collateralised by the underlying shipment, which credit conversion factor shall apply to both issuing and confirming banks |

20 per cent 3 |

||||||||||||||||||||

|

Any irrevocable undrawn commitment not included in any other specified category assigned a lower or higher credit conversion factor |

40 per cent |

||||||||||||||||||||

|

Drawn self-liquidating trade letters of credit arising from the movement of goods, that is, documentary credits collateralised by the underlying shipment, with an original maturity of one year or more |

50 per cent |

||||||||||||||||||||

|

Performance related guarantees |

50 per cent |

||||||||||||||||||||

|

Transaction-related contingent items, such as, for example, performance bonds, bid bonds, warranties and standby letters of credit |

50 per cent |

||||||||||||||||||||

|

Irrevocable note issuance facilities and irrevocable revolving underwriting facilities |

50 per cent |

||||||||||||||||||||

|

Any relevant repurchase agreement, resale agreement or asset sale with recourse in respect of which the credit risk exposure remains with the bank, which exposure amount shall be risk weighted based upon the relevant type of asset and not based upon the type of counterparty to the agreement or transaction |

100 per cent |

||||||||||||||||||||

|

Any relevant exposure arising from a securities lending/borrowing transaction or the posting of securities as collateral, where the credit risk exposure related to the securities lent or posted as collateral remains with the bank |

100 per cent |

||||||||||||||||||||

|

Any relevant exposure arising from a forward asset purchase, forward forward deposit or partly paid share or security—

|

100 per cent |

||||||||||||||||||||

|

Direct credit substitutes such as, for example, general guarantees of indebtedness, including any standby letter of credit serving as a financial guarantee, and acceptances |

100 per cent |

||||||||||||||||||||

|

Any relevant off-balance-sheet exposure rated by an eligible external credit assessment institution |

100 per cent |

||||||||||||||||||||

|

|||||||||||||||||||||

[Regulation 23(6)(g) substituted by section 2(j) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

| (h) | In the case of a securitisation exposure and resecuritisation exposure, in accordance with the relevant requirements specified below: |

| (i) | securitisation exposures will be treated differently depending on the type of the underlying exposures and/or the type of information available to the bank and in terms of the following: |

| (A) | the hierarchy of approaches for a securitisation exposure as follows: |

| (i) | For a securitisation exposure of an Internal-Ratings Based (IRB) pool as defined in this subregulation (6)(h)(i)(B), a bank must use the Securitisation Internal Ratings-Based Approach (SEC-IRBA) as described in subregulation (11)(k), unless otherwise determined by the Authority; |

| (ii) | For a securitisation exposure to a Standardised Approach (SA) pool as defined in subregulation 6(h)(i)(C), and where a bank cannot use the SEC-IRBA, it must use the Securitisation External Ratings-Based Approach (SEC-ERBA) as described in this subregulation (6)(h)(j)(l)(B) provided that— |

| (aa) | the exposure has an external credit assessment that meets the operational requirements for an external credit assessment as set out in regulation 38(6); or |

| (bb) | there is an inferred rating that meets the operational requirements for inferred ratings as set out in subregulation (6)(h)(j)(l)); |

| (iii) | A bank may use an Internal Assessment Approach (IAA) as described in subregulation (11)(g) for an unrated securitisation exposure (e.g. liquidity facilities and credit enhancements) to a SA pool within an ABCP programme provided that the bank: |

| (aa) | has supervisory approval to use the IRB approach, subject to such further requirements as may be specified in writing by the Authority from time to time, and |

| (bb) | consults with the Authority on whether and when it can apply the IAA to its securitisation exposures, especially where the bank can apply the IRB for some, but not all, underlying exposures. To ensure appropriate capital levels, there may be instances where the Authority requires a treatment other than this general rule; |

| (iv) | A bank may use the Securitisation Standardised Approach (SEC-SA) as described in this subregulation (6)(h)(j)(l) for its exposure to an SA pool if the bank cannot use the SEC-ERBA or the IAA. |

| (v) | For a securitisation exposure of a mixed pool as defined in this subregulation 6(h)(i)(D), where the bank— |

| (aa) | can calculate KIRB on at least 95% of the underlying exposure amounts of a securitisation, the bank must apply the SEC-IRBA calculating the capital charge for the underlying pool as: |

d* KIRB + (1-D)*KSA,

where:

d is the percentage of the exposure amount of underlying exposures for which the bank can calculate KIRB over the exposure amount of all underlying exposures:

KIRB is as defined in subregulation (11); and

KSA is as defined in subregulation (6)(h)(j)(l)(B);

| (bb) | cannot calculate KIRB on at least 95% of the underlying exposures, the bank must use the hierarchy for securitisation exposures of SA pools as set out in subparagraphs (ii), (iii) and (iv) above. |

| (vi) | Securitisation exposures to which none of the approaches as contemplated in this subregulation apply must be assigned a 1250% risk weight. |

| (B) | An IRB pool relates to a securitisation pool for which the bank is able to use the IRB approach to calculate capital requirements for all underlying exposures provided that – |

| (i) | the bank— |

| (aa) | has approval from the Authority to apply the IRB approach for the type of underlying exposures; and |

| (bb) | has sufficient information to calculate IRB capital requirements for these exposures; |

| (ii) | where the bank is unable to calculate capital requirements for the entire underlying pool of exposures using an IRB approach, it should be able to demonstrate to the Authority why it cannot do so; |

| (iii) | in certain cases, the Authority may prohibit a bank from treating a pool as an IRB pool in the case of particular structures or transactions, including transactions with highly complex loss allocations; tranches whose credit enhancement could be eroded for reasons other than portfolio losses; and tranches of portfolios with high internal correlations (such as portfolios with high exposure to single sectors or with high geographical concentration). |

| (C) | A SA pool relates to a securitisation pool for which the bank— |

| (i) | does not have approval to calculate IRB parameters for any underlying exposures; or |

| (ii) | is unable to calculate IRB parameters for any underlying exposures because of lack of relevant data, notwithstanding the fact that the bank has approval to calculate IRB parameters for some or all of the types of underlying exposures; or |

| (iii) | is prohibited by the Authority from treating the pool as an IRB pool as specified in sub-paragraph (6)(h)(i)(A)(i) above. |

| (D) | A mixed pool means a securitisation pool for which the bank is able to calculate IRB parameters for some, but not all, underlying exposures in a securitisation; |

| (E) | The risk-weighted exposure amount for a securitisation exposure is computed by multiplying the exposure amount, as defined in subregulation (F) below, by the appropriate risk weight determined in accordance with the hierarchy of approaches as contemplated in this subregulation 6(h)(i)(A) provided that— |

| (i) | the maximum risk weight caps for senior securitisation exposures shall be calculated in accordance with subregulation (6)(h)(iii); |

| (ii) | the maximum capital requirement for securitisation exposures, other than senior exposures as contemplated in subparagraph (i) above, may be calculated in accordance with subregulation (xvii); |

| (iii) | overlapping exposures will be risk-weighted as contemplated in subregulation (ix). |

| (F) | For purposes of subregulation (E) above, the securitisation exposure amount is the sum of the on-balance sheet amount of the exposure and the off-balance sheet exposure, where applicable, and where— |

| (i) | the on-balance sheet exposure is the carrying value, which takes into account purchase discounts and specific credit impairments raised against the securitisation exposure; |

| (ii) | the off-balance sheet exposure is calculated as follows: |

| (aa) | for credit risk mitigants sold or purchased by the bank, the bank must use the treatment set out in subregulation 7(e) read with the relevant requirements specified in subregulation (9); |

| (bb) | for derivatives contracts (other than credit derivatives contracts), such as interest rate or currency swaps sold or purchased by the bank, apply the approach used by the bank for calculating counterparty credit risk exposures as specified in subregulations (15) to (19); |

| (cc) | for facilities that are not credit risk mitigants, use a credit conversion factor of 100%. If contractually provided for, servicers may advance cash to ensure an uninterrupted flow of payments to investors provided the servicer is entitled to full reimbursement and this right is senior to other claims on cash flows from the underlying pool of exposures and in the case of any undrawn portion of servicer cash advances or facilities that is unconditionally cancellable by the said bank without prior notice, may apply a credit conversion factor of nil in respect of the said undrawn portion provided that— |

| (i) | the said facility shall duly state that the servicing agent is under no obligation to advance funds to investors or the special purpose institution in terms of the servicer cash advance facility; |

| (ii) | any cash advance made by the servicing agent shall be at the servicing agent’s sole discretion and solely to cover an unexpected temporary shortfall that arose from delayed payments; |

| (iii) | the servicing agent’s rights for reimbursement in terms of the said cash advance facility shall be senior to any other claim on cash flows arising from underlying exposures or collateral held in respect of the securitisation scheme; |

| (iv) | the undrawn amount is calculated using a conservative method; |

| (v) | a bank that acts as an originator shall in no case provide any servicer cash advance facility in respect of the securitisation scheme in respect of which that bank acts as such an originator. |

[Regulation 23 (6)(h) substituted by section 2(a) of Notice No. 2561, GG46996, dated 30 September 2022 - effective 1 October 2022]

Table 3

|

Long-term rating category 1 |

|||||

|

External credit assessment |

AAA to AA- |

A+ to A - |

BBB+ to BBB- |

BB+ to BB- 2 |

B+ and below or unrated 3 4 5 |

|

Securitisation exposure |

|||||

|

Risk weight |

20% |

50% |

100% |

350% |

1250% 3 4 |

|

Resecuritisation exposure |

|||||

|

Risk weight |

40% |

100% |

225% |

650% |

1250% 3 4 |

|

Short-term rating category 1 |

||||||||||||||

|

External credit assessment |

A-1/P-1 |

A-2/P-2 |

A-3/P-3 |

All other ratings or unrated |

||||||||||

|

Securitisation exposure |

||||||||||||||

|

Risk weight |

20% |

50% |

100% |

1250% |

||||||||||

|

Resecuritisation exposure |

||||||||||||||

|

Risk weight |

40% |

100% |

225% |

1250% 3 |

||||||||||

|

||||||||||||||

[Regulation 23(6)(h)(i), Table 3, substituted by regulation 6(e) of Notice No. 297, GG 40002, dated 20 May 2016]

| (ii) | [Regulation 23 (6)(h)(ii) deleted by section 2(b) of Notice No. 2561, GG46996, dated 30 September 2022 - effective 1 October 2022] |

Table 4

|

Nature of exposure |

Credit conversion factor |

|

Most senior position in an unrated structure |

Refer to subparagraph (iii) below |

|

Any unrated second loss position provided by a bank that acts as a sponsor in respect of an ABCP programme |

Refer to subparagraph (iv) below |

|

First-loss credit enhancement facilities |

Refer to subparagraph (v) below |

|

Second-loss credit enhancement facilities |

Refer to subparagraph (vi) below |

|

Eligible liquidity facilities |

Refer to subparagraph (vii) below |

|

Eligible servicer cash advance facilities |

Refer to subparagraph (viii) below |

|

Facilities that overlap |

Refer to subparagraph (ix) below |

|

Securitisation of revolving facilities with early amortisation features |

Refer to subparagraph (xi) below |

|

Any other rated exposure |

100 per cent |

|

Other exposures |

100 per cent |

| (iii) | In the case of a senior securitisation exposure— |

| (A) | a bank may apply a “look-through” approach to a senior securitisation exposure, whereby the senior securitisation exposure could receive a maximum risk weight equal to the exposure weighted-average risk weight applicable to the underlying exposures, provided that— |

| (i) | the bank has knowledge of the composition of the underlying exposures at all times; |

| (ii) | the applicable risk weight under the IRB framework would be calculated inclusive of the expected loss portion multiplied by 12.5; |

| (iii) | where the bank uses exclusively the SA or the IRB approach, the risk weight cap for senior exposures would equal the exposure weighted-average risk weight that would apply to the underlying exposures under the SA or IRB framework, respectively; |

| (iv) | in the case of mixed pools, when applying the SEC-IRBA, the SA part of the underlying pool would receive the corresponding SA risk weight, while the IRB portion would receive IRB risk weights; when applying the SEC-SA or the SEC-ERBA, the risk weight cap for senior exposures would be based on the SA exposure weighted-average risk weight of the underlying assets, whether or not they are originally IRB; |

| (v) | where the risk weight cap results in a lower risk weight than the floor risk weight of 15%, the risk weight resulting from the cap must be used. |

| (B) | For purposes of sub-paragraph (A) a securitisation exposure is considered to be a senior exposure, and consequently the senior tranche, if it is effectively backed or secured by a first claim on the entire amount of the assets in the underlying securitisation pool (and does not include other claims that in a technical sense may be more senior in the waterfall such as a swap claim), |

Provided that:

| (i) | if a senior tranche is retranched or partially hedged, that is not on a pro rata basis, only the new senior part would be treated as senior for capital purposes; |

| (ii) | different maturities of several senior tranches that share pro rata loss allocation and therefore benefit from the same level of credit enhancement, shall have no effect on the seniority of these tranches. |

For example,

| (i) | In a typical synthetic securitisation, an unrated tranche would be treated as a senior tranche, provided that all of the conditions for inferring a rating from a lower tranche that meets the definition of a senior tranche are fulfilled. |

| (ii) | In a traditional securitisation where all tranches above the first-loss piece are rated, the most highly rated position would be treated as a senior tranche. When there are several tranches that share the same rating, only the most senior tranche in the cash flow waterfall would be treated as senior (unless the only difference among them is the effective maturity). In addition, when the different ratings of several senior tranches only result from a difference in maturity, all of these tranches should be treated as a senior tranche. |

Usually, a liquidity facility supporting an ABCP programme would not be the most senior position within the programme; the commercial paper, which benefits from the liquidity support, typically would be the most senior position. However, a liquidity facility may be viewed as covering all losses on the underlying receivables pool that exceed the amount of over collateralisation/reserves provided by the seller and as being most senior if it is sized to cover all of the outstanding commercial paper and other senior debt supported by the pool, so that no cash flows from the underlying pool could be transferred to the other creditors until any liquidity draws were repaid in full. In such a case, the liquidity facility can be treated as a senior exposure. Otherwise, if these conditions are not satisfied, or if for other reasons the liquidity facility constitutes a mezzanine position in economic substance rather than a senior position in the underlying pool, the liquidity facility should be treated as a non-senior exposure.

[Regulation 23 (6)(h)(iii) substituted by section 2(c) of Notice No. 2561, GG46996, dated 30 September 2022 - effective 1 October 2022]

| (iv) | [Regulation 23(6)(h)(iv) deleted by section 2(b) of Notice No. 2561, GG46996, dated 30 September 2022 - effective 1 October 2022] |

| (v) | In the case of a first-loss credit enhancement facility the bank shall risk weight the relevant exposure amount in accordance with the relevant requirements specified in paragraph (j) below; |

| (vi) | [Regulation 23 (6)(h)(vi) deleted by section 2(b) of Notice No. 2561, GG46996, dated 30 September 2022 - effective 1 October 2022] |

| (vii) | In the case of eligible liquidity facilities, that is, a facility that complies with the conditions specified in paragraph 7 of the exemption notice relating to securitisation schemes, a bank that acts as an originator shall in no case provide any liquidity facility in respect of the securitisation scheme in respect of which that bank acts as such an originator. |

[Regulation 23 (6)(h)(iv) substituted by section 2(d) of Notice No. 2561, GG46996, dated 30 September 2022 - effective 1 October 2022]

| (A) | When a bank or another institution within a banking group of which such a bank is a member, acting as a servicing agent, a repackager or a sponsor in respect of a securitisation scheme or resecuritisation exposure, provides an eligible liquidity facility in respect of such a securitisation scheme, that is, a facility that complies with the conditions specified in paragraph 7 of the exemption notice relating to securitisation schemes, the said bank or institution shall in the case of— |

| (i) | a facility with an external rating apply to the said position a credit-conversion factor of 100 per cent and the risk weight relating to the specific rating, as specified in subparagraph (i) above; |

| (ii) | a facility other than a facility with an external rating, irrespective of the maturity of the facility, apply a credit-conversion factor of 50 per cent in respect of the said eligible liquidity facility, which credit-conversion factor shall be applied to the highest risk weight assigned to any of the underlying individual exposures covered by the liquidity facility. |

[Regulation 23(6)(h)(vii)(A) substituted by regulation 2(c) of Notice No. R. 261, GG 38616, dated 27 March 2015]

| (B) | When a bank that provides a liquidity facility in respect of a traditional or synthetic securitisation scheme does not comply with the conditions specified in this subparagraph (vii) and the conditions specified in paragraph 7 of the exemption notice relating to securitisation schemes, the liquidity facility concerned— |

| (i) | shall be regarded as a first-loss credit-enhancement facility provided to the scheme by the aforementioned bank; and |

| (ii) | shall be risk weighted in accordance with the relevant requirements specified in subparagraph (v) above, |

provided that the aggregate amount of capital maintained by the said bank in terms of this item (B) shall be limited to the amount of capital that the bank would have been required to maintain in respect of all the assets or credit risk inherent in the assets transferred to the special-purpose institution in terms of the securitisation scheme if the said assets or credit risk inherent in the assets were actually held on the balance sheet of the bank that provided the said liquidity facility.

| (viii) | [Regulation 23 (6)(h)(viii) deleted by section 2(b) of Notice No. 2561, GG46996, dated 30 September 2022 - effective 1 October 2022] |

(ix) For calculating the capital requirement for overlapping exposures—

| (A) | the bank’s exposure A overlaps another exposure B if in all circumstances the bank will preclude any loss for the bank on exposure B by fulfilling its obligations with respect to exposure A. |

For example, if a bank provides full credit support to some notes and holds a portion of these notes, its full credit support obligation precludes any loss from its exposure to the notes. If a bank can verify that fulfilling its obligations with respect to exposure A will preclude a loss from its exposure to B under any circumstance, the bank does not need to calculate risk-weighted assets for its exposure to B.

| (B) | To determine the overlap, a bank may, for the purposes of calculating capital requirements, split or expand its exposures, that is— |

| (i) | splitting exposures into portions that overlap with another exposure held by the bank and other portions that do not overlap; and |

| (ii) | expanding exposures by assuming for capital purposes that obligations with respect to one of the overlapping exposures are larger than those established contractually. This could be done, for instance, by expanding either the trigger events to exercise the facility and/or the extent of the obligation. |

For example, a liquidity facility may not be contractually required to cover defaulted assets or may not fund an ABCP programme in certain circumstances. For capital purposes, such a situation would not be regarded as an overlap to the notes issued by that ABCP conduit. However, the bank may calculate risk-weighted assets for the liquidity facility as if it were expanded (either in order to cover defaulted assets or in terms of trigger events) to preclude all losses on the notes. In such a case, the bank would only need to calculate capital requirements on the liquidity facility.

| (C) | An overlap could also be recognised between relevant capital charges for exposures in the trading book and capital charges for exposures in the banking book, provided that the bank is able to calculate and compare the capital charges for the relevant exposures ; |

[Regulation 23 (6)(h)(ix) substituted by section 2(e) of Notice No. 2561, GG46996, dated 30 September 2022 - effective 1 October 2022]

| (xi) | In case of securitisation transactions containing early amortisation provisions: |

| (A) | Where the securitisation transaction contains one of the following examples as set out in subparagraphs (i) to (iv) below and meets the conditions specified in paragraph 4 for traditional securitisations and paragraph 5 for synthetic securitisations of the exemption notice for securitisation schemes, an originating bank may exclude the underlying exposures associated with such a transaction from the calculation of risk weighted exposure, but must still hold regulatory capital against any securitisation exposures they retain in connection with the transaction: |

| (i) | a replenishment structure, in terms of which structure the underlying exposures are not of a revolving nature and the early amortisation terminates the ability of the bank to transfer any further exposures; |

| (ii) | a transaction in respect of revolving assets, which transaction contains early amortisation features that mimic a term structure, that is, the risk relating to the underlying facilities does not return to the originator and where the early amortisation provision in a securitisation of revolving credit facilities does not effectively result in subordination of the originator’s interest; |

| (iii) | a structure in terms of which the bank securitised one or more revolving credit facilities but the investors remain fully exposed to any future draws by the borrowers, even after an early amortisation event has occurred; or |

| (iv) | the early amortisation provision is solely triggered by events unrelated to the performance of the underlying assets or the bank that transferred the assets, such as material changes in tax laws or regulations. |

| (B) | A securitisation transaction is deemed not to meet the conditions specified in paragraph 4 for traditional securitisations and paragraph 5 for synthetic securitisations of the exemption notice for securitisation schemes if— |

| (i) | a bank acts as an originator or sponsor to a securitisation transaction that includes one or more revolving credit facilities; and |

| (ii) | the securitisation transaction incorporates an early amortisation or similar provision that, if triggered, would— |

| (aa) | subordinate the bank’s senior or pari passu interest in the underlying revolving credit facilities to the interest of other investors; |

| (bb) | subordinate the bank’s subordinated interest to an even greater degree relative to the interests of other parties; or |

| (cc) | in other ways increases the bank’s exposure to losses associated with the underlying revolving credit facilities. |

[Regulation 23(6)(h)(xi) substituted by section 2(f) of Notice No. 2561, GG46996, dated 30 September 2022 - effective 1 October 2022]

| (xii) | The maximum capital requirements for a securitisation exposure is as follows: |

| (A) | A bank (acting as an originator, sponsor or investor) using the SEC-IRBA for a securitisation exposure may apply a maximum capital requirement for the securitisation exposures it holds equal to the IRB capital requirement (including the expected loss portion) that would have been assessed against the underlying exposures had they not been securitised and treated under the appropriate sections of the IRB framework as well as subregulations 23(21) and (22); |

| (B) | An originating or sponsor bank using the SEC-ERBA or SEC-SA for a securitisation exposure may apply a maximum capital requirement for the securitisation exposures it holds equal to the capital requirement that would have been assessed against the underlying exposures had they not been securitised; |

| (C) | In the case of mixed pools, the maximum capital requirement should also be calculated by adding up the capital before securitisation; that is, by adding up the capital required under the general credit risk framework for the IRB and the SA part of the underlying pool, respectively. The IRB part of the capital requirement includes the expected loss portion; |

| (D) | Notwithstanding the approach adopted by the bank to calculate its capital requirements for a securitisation exposure, a bank will need the following inputs in order to apply a maximum capital charge to a bank’s securitisation exposure: |

| (i) | The largest proportion of interest that the bank holds for each tranche of a given pool (P). In particular: |

| (aa) | For a bank that has one or more securitisation exposure(s) that reside in a single tranche of a given pool, P equals the proportion (expressed as a percentage) of securitisation exposure(s) that the bank holds in that given tranche (calculated as the total nominal amount of the bank’s securitisation exposure(s) in the tranche) divided by the nominal amount of the tranche. |

| (bb) | For a bank that has securitisation exposures that reside in different tranches of a given securitisation, P equals the maximum proportion of interest across tranches, where the proportion of interest for each of the different tranches should be calculated as described above. |

| (ii) | Capital charge for underlying pool (KP): |

| (aa) | For an IRB pool, KP equals KIRB as defined in subregulation (11)(k); |

| (bb) | For an SA pool, KP equals KSA as defined in subregulation (6)(h)(j)(l)(B); |

| (cc) | For a mixed pool, KP equals the exposure weighted average capital charge of the underlying pool using KSA for the proportion of the underlying pool for which the bank cannot calculate KIRB, and KIRB for the proportion of the underlying pool for which a bank can calculate KIRB. |

| (iii) | The maximum aggregated capital requirement for a bank’s securitisation exposures in the same transaction will be equal to KP * P. |

| (E) | In applying the maximum capital charge cap, the entire amount of any gain on sale and credit-enhancing interest-only strips arising from the securitisation transaction must be deducted in accordance with regulation 38(5)(a)(i)(F). |

[Regulation 23(6)(h)(xii) inserted by section 2(g) of Notice No. 2561, GG46996, dated 30 September 2022 - effective 1 October 2022]

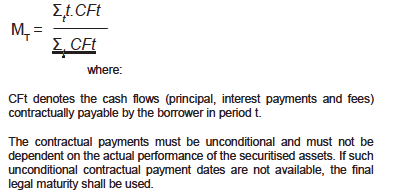

| (xiii) | Tranche maturity |

| (A) | For risk-based capital purposes as contemplated in the SEC-IRBA as set out in subregulation (11)(k) or the SEC-ERBA as set out in subregulation (6)(k), the tranche maturity (MT) is the tranche’s remaining effective maturity in years, with a floor of one year and a cap of five years provided that— |

| (i) | the tranche maturity can be measured at the bank's discretion in either of the following matters: |

| (aa) | As the rand-weighted-average maturity of the contractual cash flows of the tranche: |

| (bb) | On the basis of final legal maturity of the tranche, as: |

MT = (ML - 1) * 80%,

where:

ML is the final legal maturity of the tranche.

| (ii) | when determining the maturity of a securitisation exposure, banks must take into account the maximum period of time it will be exposed to potential losses from the securitised assets— |

| (aa) | in cases where a bank provides a commitment, the bank must calculate the maturity of the securitisation exposure resulting from this commitment as the sum of the contractual maturity of the commitment and the longest maturity of the asset(s) to which the bank would be exposed after a draw has occurred. If those assets are revolving, the longest contractually possible remaining maturity of the asset that might be added during the revolving period would apply, rather than the (longest) maturity of the assets currently in the pool; |

| (bb) | in cases where risk of the commitment/protection provider is not limited to losses realised until the maturity of that instrument (e.g. total return swaps), the same treatment applies as per subparagraph (aa) above; |

| (cc) | in cases where the credit protection instruments are only exposed to losses that occur up to the maturity of that instrument, a bank may apply the contractual maturity of the instrument and would not be required to look through to the protected position. |

[Regulation 23(6)(h)(xiii) inserted by section 2(h) of Notice No. 2561, GG46996, dated 30 September 2022 - effective 1 October 2022]

| (i) | In the case of all unsettled securities or derivative contracts subject to counterparty risk, in accordance with the relevant provisions specified in subregulations (15) to (19) below. |

| (j) | In the case of all other exposures, in accordance with the relevant requirements specified in table 1 below: |

|

Table 1 |

|||||||||||

|

Risk weight |

Transactions with the following counterparties, including assets |

||||||||||

|

0% |

Transactions with the following counterparties Central government of the RSA, provided that the relevant exposure is repayable and funded in Rand Reserve Bank, provided that the relevant exposure is repayable and funded in Rand Corporation for Public Deposits, provided that the relevant exposure is repayable and funded in Rand Bank for International Settlements (BIS) International Monetary Fund (IMF) European Central Bank (ECB) European Stability Mechanism (ESM) European Financial Stability Facility (EFSF) European Union World Bank Group, including the International Bank for Reconstruction and Development (IBRD) and the International Finance Corporation (IFC) Multilateral Investment Guarantee Agency (MIGA) International Development Association (IDA) Asian Development Bank (ADB) African Development Bank (AfDB) European Bank for Reconstruction and Development (EBRD) Inter-American Development Bank (IADB) European Investment Bank (EIB) European Investment Fund (EIF) Nordic Investment Bank (NIB) Caribbean Development Bank (CDB) Islamic Development Bank (IDB) Council of Europe Development Bank (CEDB) International Finance Facility for Immunization (IFFIm) Asian Infrastructure Investment Bank (AIIB) Intragroup bank balances 1 Intragroup balances with other formally regulated financial entities with capital requirements similar to these Regulations 1 Intragroup balances with branches of foreign banks

Assets Cash and cash equivalents such as gold bullion owned by the bank |

||||||||||

|

|||||||||||

|

20% |

Transactions with the following counterparties, including assets Transactions with the following counterparties

RSA public-sector bodies, excluding exposures to the central government, SA Reserve Bank and the Corporation for Public Deposits when the said exposure is repayable and funded in Rand Banks in the RSA, provided that the claim on the bank has an original maturity of three months or less and is denominated and funded in Rand, excluding any claim on a RSA bank that is renewed or rolled resulting in an effective maturity of more than three months A securities firm in the RSA, provided that such a firm is subject to comparable supervisory and regulatory arrangements than banks in the RSA, including, in particular, risk-based capital requirements and regulation and supervision on a consolidated basis and the claim on the securities firm has an original maturity of three months or less and is denominated and funded in Rand, excluding any claim on a securities firm in the RSA that is renewed or rolled resulting in an effective maturity of more than three months

Assets Cash items in process of collection |

||||||||||

|

100% |

Transactions with the following counterparties or assets

An investment in a significant minority or majority owned or controlled commercial entity, which investment amounts to less than 15 per cent of the issued common equity tier 1 capital and reserve funds, additional tier 1 capital and reserve funds and tier 2 capital and reserve funds of the reporting bank, as reported in items 41, 65 and 78 of form BA 700

Any other exposure to a counterparty or asset not specifically covered elsewhere in paragraphs (a) to (i) hereinbefore, or in this paragraph (j) |

||||||||||

|

150% 1 |

Assets Subordinated debt or any other type of instrument that meets the requirements specified in the Act read with the Regulations, related to qualifying tier 2 capital or any relevant other TLAC liability, other than—

respectively envisaged below, issued by any corporate entity or person, or any bank |

||||||||||

|

250% 1; 2 |

Equity or any other type of instrument that meets the requirements specified in the Act read with the Regulations, related to qualifying common equity tier 1 capital or additional tier 1 capital, other than speculative unlisted equity envisaged below, issued by any corporate entity or person, or any bank |

||||||||||

|

400% 1; 3 |

Speculative unlisted equity acquired or held for short-term resale purposes or that constitutes venture capital or any similar investment subject to price volatility and acquired in anticipation of significant future capital gain, held in any unlisted company |

||||||||||

|

150% or higher 4 |

Any other asset or instrument specified in writing by the Authority |

||||||||||

|

Risk weight |

Transactions with the following counterparties, including assets |

||||||||||

|

|

Equity investments in funds 5 |

||||||||||

|

|||||||||||

|

Risk weight |

Transactions with the following counterparties, including assets |

|

1250% |

A first-loss position, including a credit enhancement facility in respect of a securitisation or resecuritisation scheme. The relevant amount up to a materiality threshold specified in a guarantee or credit-derivative contract, which materiality threshold either reduces the amount of payment or requires a given amount of loss to occur for the account of the protection buyer before the protection seller is obliged to make payment to the said protection buyer. The excess amount relating to a significant investment, that is, a shareholding of 20 per cent or more, in a commercial entity, which investment is equal to or exceeds 15 per cent of the issued common equity tier 1 capital and reserve funds, additional tier 1 capital and reserve funds and tier 2 capital and reserve funds of the reporting bank, as reported in items 41, 65 and 78 of the form BA 700. The relevant excess amount when the aggregate amount of significant investments, that is, a shareholding of 20 per cent or more, in commercial entities, exceeds 60 per cent of the sum of the issued common equity tier 1 capital and reserve funds, additional tier 1 capital and reserve funds and tier 2 capital and reserve funds of the reporting bank, as reported in items 41, 65 and 78 of the form BA 700. Credit protection provided, which credit protection has a long-term rating of B+ or below or a short-term rating other than A-1/P-1, A-2/P-2 or A-3/P-3. Any unrated position in a rated structure relating to credit protection provided in terms of a credit-derivative instrument. In the case of a synthetic securitisation scheme, any retained position that is unrated or rated below investment grade. The net amount, that is, the amount after any specific credit impairment or provision, and any deduction directly against common equity tier 1 or additional tier 1 capital and reserve funds, have been taken into account, in respect of any credit enhancing interest-only strip relating to a securitisation transaction. |

[Regulation 23(6)(j) substituted by section 2(k) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

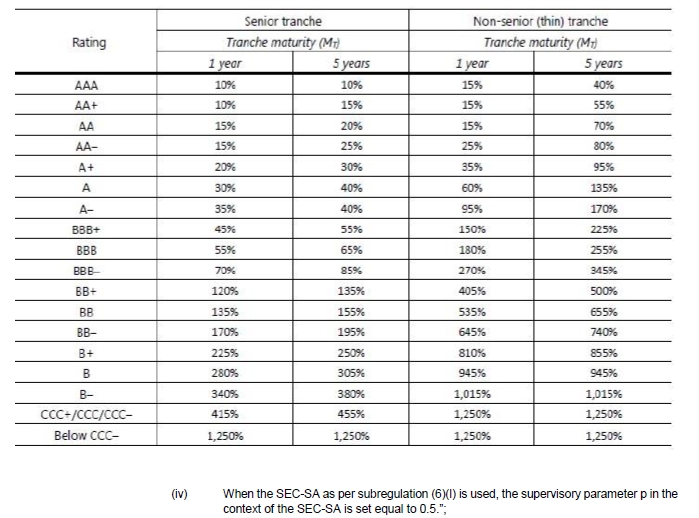

SEC-ERBA

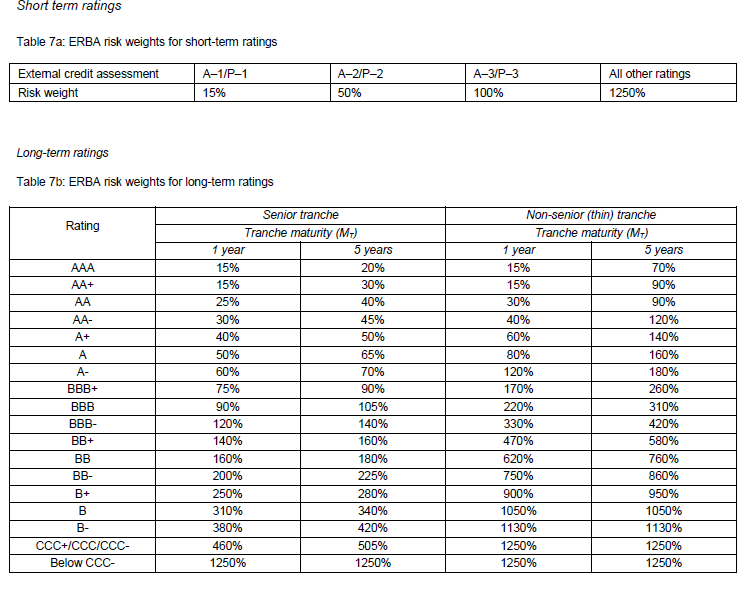

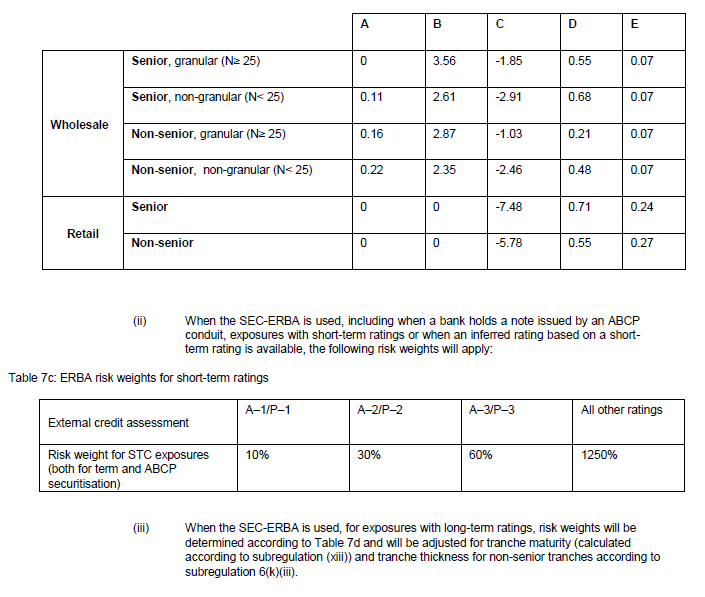

| (k) | For securitisation exposures that are externally rated, or for which an inferred rating is available, and provided that the operational requirements as contemplated in regulation 38(6) and subregulation (xv) below are satisfied, the risk-weighted assets under the SEC-ERBA must be determined by multiplying securitisation exposure amounts as contemplated in subregulation 6(h)(i)(F) above by the appropriate risk weights as determined below: |

| (i) | in the case of an exposure with an external short-term credit rating, or when an inferred rating based on an external short-term credit rating is available, use the risk weights specified in Table 7(a) below; |

| (ii) | in the case of an exposure with an external long-term credit rating, or when an inferred rating based on an external long-term credit rating is available use the risk weights specified in Table 7(b), where the risk weights depend on: |

| (A) | the external rating grade or an available inferred rating; |

| (B) | the seniority of the position; |

| (C) | the tranche maturity as calculated in terms of subregulation (6)(h)(xiii) and using linear interpolation between the risk weight for one and five years; and |

| (D) | the tranche thickness for non-senior tranches, as calculated in terms of subparagraph (iii) below |

| (iii) | To account for tranche thickness, banks shall calculate the risk weight for non-senior tranches as follows: |

Risk weight = [risk weight from table 7b after adjusting for maturity] * [1 – min(T; 50%)],

where T equals tranche thickness, and is measured as the tranche detachment point D minus the tranche attachment point A, as defined respectively, in subregulation (23)(6)(j) and 23(6)(m).

| (iv) | In the case of market risk hedges such as currency or interest rate swaps, the risk weight will be inferred from a securitisation exposure that is pari passu to the swaps or, if such an exposure does not exist, from the next subordinated tranche. |

| (v) | The resulting risk weight is subject to a floor risk weight of 15%. In addition, the resulting risk weight should never be lower than the risk weight corresponding to a senior tranche of the same securitisation with the same rating and maturity. |

| (vi) | In accordance with the hierarchy of approaches as determined in accordance with subregulation (6)(h)(i)(A), a bank may infer a rating for an unrated position and use the SEC-ERBA provided that the following requirements are met— |

| (A) | the reference securitisation exposure shall in all respects rank pari passu or be subordinated to the relevant unrated securitisation exposure; |

| (B) | the bank shall take into account any relevant credit enhancement when the bank assesses the relative subordination of the unrated exposure in relation to the reference securitisation exposure. For example, when the reference securitisation exposure benefits from any third-party guarantee or other credit enhancement, which protection is not available to the unrated exposure, the bank shall not assign an inferred rating to the said unrated exposure; |

| (C) | the maturity of the reference securitisation exposure shall be equal to or longer than the maturity of the relevant unrated exposure; |

| (D) | on a continuous basis, the bank shall update any inferred rating in order to reflect any subordination of the unrated position or changes in the external rating of the reference securitisation exposure; and |

| (E) | the external rating of the reference securitisation exposure shall comply with the relevant requirements for recognition of external ratings specified in regulation 38(6) of these Regulations. |

[Regulation 23(6)(k) inserted by section 2(i) of Notice No. 2561, GG46996, dated 30 September 2022 - effective 1 October 2022]

SEC-SA

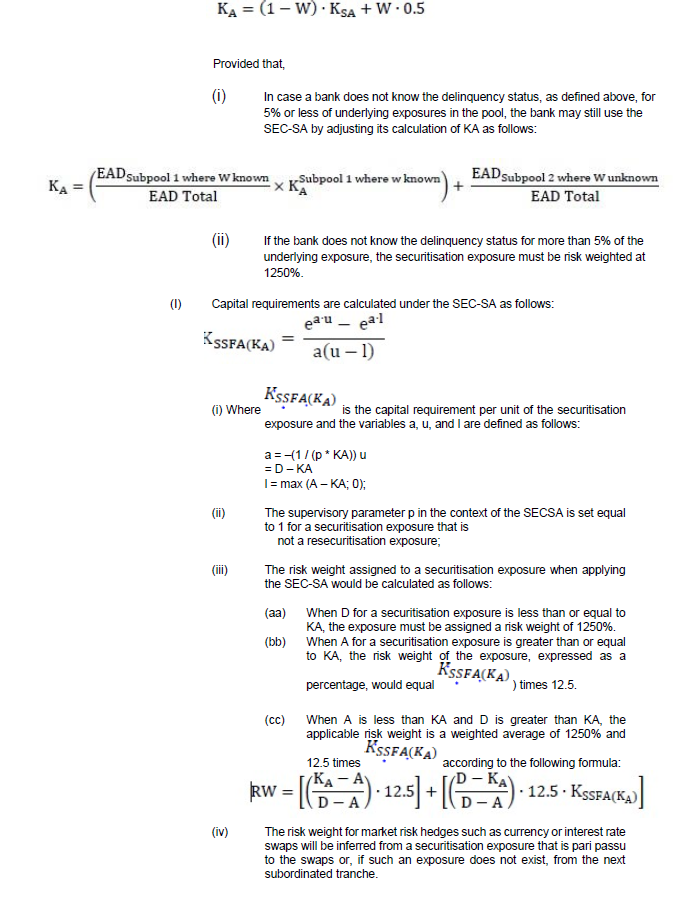

| (l) | When a bank cannot use the SEC-IRBA or the SEC-ERBA, it must use the SEC-SA in order to calculate capital requirements for a securitisation exposure to a SA pool in accordance with the relevant requirements specified below: |

| (A) | In order to use the SEC-SA a bank would use a supervisory formula and the following bank-supplied inputs: |

| (i) | the SA capital charge had the underlying exposures not been securitised (KSA); |

| (ii) | the ratio of delinquent underlying exposures to total underlying exposures in the securitisation pool (W) as defined in subparagraph (F) below; and |