| (i) |

Subject to such conditions as may be specified in writing by the Authority, a bank that adopted the advanced IRB approach for the measurement of the bank’s exposure to credit risk shall adopt and apply the said approach in respect of all material eligible asset classes and business units. |

[Regulation 23(13)(b)(i) substituted by section 2(kkkkkk) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

| (ii) |

For a minimum period of three years prior to a bank's implementation of the advanced IRB approach for the measurement of the bank's exposure to credit risk, the rating and risk estimation systems and processes of the bank should have— |

[Subparagraph (ii) of subregulation (13)(b) substituted by regulation 2(dd) of Notice No. R. 261 dated 27 March 2015]

(A) provided a meaningful assessment of borrower and transaction characteristics;

| (B) |

provided a meaningful differentiation of risk; |

| (C) |

provided materially accurate and consistent quantitative estimates of risk, including PD ratios, LGD ratios and EAD amounts; |

| (D) |

produced internal ratings and default and loss estimates that formed an integral part of the bank's— |

| (i) |

credit approval process; |

| (ii) |

risk management process; |

| (iii) |

internal capital allocation process; |

| (iv) |

corporate governance process; |

| (E) |

been subjected to appropriate independent review; |

| (F) |

been broadly in compliance with the relevant minimum requirements specified in subregulation (11) above; |

[Regulation 23(13)(b)(ii)(F) substituted by regulation 6(w) of Notice No. R. 297, GG 40002, dated 20 May 2016]

| (G) |

been broadly in compliance with the relevant minimum requirements relating to own estimates of LGD and EAD specified in this subregulation (13). |

[Regulation 23(13)(b)(ii)(G) inserted by regulation 2(ee) of Notice No. R. 261 dated 27 March 2015]

| (iii) |

A facility rating of a bank that adopted the advanced IRB approach for the measurement of the bank's exposure to credit risk shall exclusively reflect the LGD ratio of the particular exposure, provided that— |

| (A) |

a facility rating shall include all factors that may have an influence on the LGD ratio, such as the type of collateral, the product, the industry or the purpose; |

| (B) |

any borrower characteristics shall be included as LGD rating criteria only to the extent that such characteristics are predictive of LGD; |

| (C) |

the bank shall maintain a sufficient number of facility grades in order to avoid the grouping of facilities with widely varying LGD ratios into a single grade. |

| (iv) |

A bank that adopted the advanced IRB approach for the measurement of the bank's exposure to credit risk shall in the case of exposures to corporate institutions, sovereigns and banks collect and store data in respect of— |

| (A) |

the LGD ratios and EAD estimates associated with each relevant facility; |

| (B) |

the key data that was used to derive a particular risk estimate; |

| (C) |

the person or model responsible for a particular risk estimate; |

| (D) |

the estimated and realised LGD ratios and EAD amounts associated with each relevant defaulted facility; |

| (E) |

the credit risk mitigating effects of guarantees or credit-derivative instruments on LGD ratios, that is, the bank shall retain data in respect of the LGD ratio of the facility before and after the effect of a guarantee or credit-derivative instrument was taken into consideration; |

| (F) |

the components of loss or recovery for each defaulted exposure such as the amounts recovered, the source of recovery, for example, collateral, liquidation proceeds and guarantees, the time period required for recovery and administrative costs. |

Unless specifically otherwise provided in this subregulation (13), a bank that adopted the advanced IRB approach for the measurement of the bank's exposure to credit risk—

| (A) |

shall in the case of exposures to corporate institutions, sovereigns or banks estimate a PD ratio in respect of each internal borrower grade, which PD estimate shall comply with the relevant minimum requirements specified in subregulation (11)(b)(vi)(A) above; |

| (B) |

shall in the case of retail exposures estimate a PD ratio in respect of each relevant retail pool of exposures, which PD estimate shall comply with the relevant minimum requirements specified in subregulation (11)(b)(vi)(B) above; |

[Regulation 23(13)(b)(v)(B) substituted by section 2(llllll) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

| (C) |

shall estimate an appropriate LGD ratio in respect of all relevant facilities and asset classes, which LGD ratio— |

| (i) |

shall incorporate all relevant and material data and information, including conditions relating to an economic downturn when such information is necessary to duly capture the relevant risk; |

| (ii) |

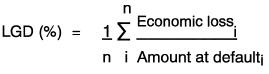

shall not be less than the long-run default-weighted average loss rate given default, based on the average economic loss of all observed defaults within the data source for a particular type of facility, which default-weighted average loss rate given default shall be calculated in accordance with the formula specified below: |

For example, when a bank's pool of defaulted exposures consists of 75 defaults where the exposure at default is R10 000 and the bank suffered a complete loss, that is, an LGD ratio of 100%, and 25 defaults where the exposure at default was R1 000 000 but the bank lost only R200 000, that is, an LGD ratio of 20%, the bank's default-weighted average LGD shall be calculated as:

| (iii) |

shall be based on the definition of default, specified in regulation 67; |

| (iv) |

may be based on averages of loss severities observed during periods of high credit losses, obtained from internal and/or external data, provided that the data shall be representative of long run experience; |

| (v) |

shall appropriately incorporate any potential correlation or dependence between the risk relating to the borrower and the collateral, collateral provider or protection provider. |

When the bank’s estimate of LGD takes the existence of collateral into account, the bank shall ensure that it establishes sufficiently robust internal policies, processes and procedures related to collateral management, operational procedures, legal certainty and risk management process that are in all material respects commensurate to the relevant requirements specified in subregulation (9)(b) read with subregulation (12)(b);

[Regulation 23(13)(b)(v)(C)(v) substituted by section 2(mmmmmm) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

| (vi) |

shall incorporate the effect of a currency mismatch between the underlying obligation and any collateral obtained; |

| (vii) |

shall be based on historical recovery rates and empirical evidence and not, for example, solely on the estimated market value of collateral; |

| (viii) |

shall be based on a population of exposures that closely matches or is at least comparable to the bank's existing exposures and lending standards; |

| (ix) |

shall be based on economic and market conditions that are relevant and current; |

| (x) |

shall be based on a sufficient number of exposures and data periods that will ensure accurate and robust LGD estimates; |

| (xi) |

shall be based on an estimation technique that performs well in out-of-sample tests; |

| (xii) |

shall be reviewed on a regular basis but not less frequently than once a year, or when material new information is obtained; |

| (xiii) |

shall in the case of— |

| (aa) |

defaulted assets reflect the possibility that the bank may have to recognise additional, unexpected losses during the recovery period; |

| (bb) |

exposures to corporate institutions, sovereigns or banks be based on a minimum data observation period that covers a complete economic cycle, but which observation period shall in no case be less than seven years in respect of at least one of the bank’s data sources; |

[Regulation 23(13)(b)(v)(C)(xiii)(bb) substituted by section 2(nnnnnn) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

| (cc) |

retail exposures be based on a minimum data observation period of no less than five years, provided that— |

| (i) |

when the available observation period for any of the relevant sources spans a period of more than five years, and the data are relevant, the bank shall use that longer period of available data; |

| (ii) |

in all relevant cases, the data shall include an appropriate and representative mix of good and bad years of the economic cycle relevant for the portfolio; |

[Regulation 23(13)(b)(v)(C)(xiii)(cc) substituted by section 2(oooooo) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

| (dd) |

unsecured corporate exposure be subject to an LGD floor of 25 per cent, whenever the bank calculates its expected and/or unexpected loss amount for purposes of these Regulations, |

[Regulation 23(13)(b)(v)(C)(xiii)(dd) inserted by section 2(pppppp) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

Provided that when the bank complies with the respective requirements specified in this subregulation (13) for the calculation of its own internal estimates of LGD for a pool of unsecured exposures and the bank obtains eligible collateral against one of those exposures, but the bank is unable to model the effects of the collateral since the bank, for example, may not have enough data to model the effect of the collateral on recoveries, the bank may choose to apply either the formula specified in subregulation (12)(b)(iii) or subregulation (12)(c), with the exception that the variable LGDU shall in all relevant cases be the bank’s own internal estimate of the unsecured LGD, provided that that estimate of LGDU has not already taken into account the effects of any collateral recoveries.

[Regulation 23(13)(b)(v)(C)(xiii) proviso inserted by section 2(qqqqqq) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

| (D) |

shall estimate an appropriate EAD amount in respect of all relevant eligible or permitted facilities, commitments to extend credit or asset classes, which EAD amount— |

| (i) |

shall in the case of— |

| (aa) |

on-balance-sheet items be no less than the current drawn amount after the effect of set-off in terms of the provisions of regulation 13 has been taken into consideration; |

| (bb) |

any undrawn revolving commitment to extend credit, that is, any loan facility in terms of which the borrower has the flexibility to decide how often to withdraw from the loan facility and at what time intervals, to prepay or repay and redraw loan amounts at the borrower’s discretion, be equal to the bank’s own internal estimate of EAD unless the commitment is subject to a CCF of 100 per cent in terms of the foundation IRB approach, in which case the bank shall apply the said CCF of 100 per cent; |

| (cc) |

any off-balance sheet item other than an undrawn revolving commitment to extend credit, be equal to the relevant undrawn non-revolving commitment multiplied with the relevant credit conversion factor specified in subregulation (6) read with subregulation (8); |

| (dd) |

all relevant off-balance sheet items and any related credit conversion factors be effectively quarantined from the potential effects of instability that may be associated with borrower facilities close to being fully drawn at the relevant reference dates, particularly when the bank makes use of the so-called undrawn limit factor (ULF) approach or similar approaches to estimate its CCFs; |

| (ee) |

derivative instruments or transactions that expose the bank to counterparty credit risk be calculated in accordance with the relevant directives and requirements specified in subregulations (15) to (19); |

| (ff) |

exposures to corporate institutions, sovereigns or banks be based upon a complete economic cycle, provided that— |

| (i) |

the time period on which the EAD amount is based shall in no case be less than seven years; |

| (ii) |

the EAD estimates shall be based on a default-weighted average and not a time-weighted average amount; |

| (gg) |

retail exposures be based upon a data observation period of no less than five years, provided that the bank may with the prior written approval of the Authority place more reliance on recent data when the said data better reflect likely draw-downs in respect of the bank’s retail exposures; |

| (ii) |

shall be an estimate of the long-run default-weighted average EAD amounts in respect of similar eligible facilities and borrowers over a sufficiently long period of time; |

| (iii) |

shall appropriately incorporate any correlation between the default frequency and the extent of EAD amounts; |

| (iv) |

shall appropriately incorporate the effects of downturns in the economy, that is, the risk drivers of the bank’s internal model or the bank’s internal data or external data shall incorporate the cyclical nature of each facility; |

| (aa) |

a 12-month fixed-horizon approach, that is, for each relevant observation in the reference data set, the bank’s default outcomes shall be linked to relevant obligor and facility characteristics twelve months prior to default; |

| (bb) |

a population of exposures that closely matches or is at least comparable to the bank’s existing exposures and lending standards; |

| (cc) |

a sufficient number of exposures and data periods that will ensure accurate and robust estimates of EAD amounts; |

| (dd) |

economic and market conditions that are relevant and current; |

| (ee) |

criteria that are plausible and intuitive; |

| (ff) |

reference data that appropriately reflects the obligor, facility and bank management practice characteristics of the respective eligible exposures to which the estimates are applied, that is, EAD estimates applied to particular eligible exposures shall, for example, not be based on data that comingle the effects of disparate characteristics or data from exposures that exhibit different characteristics, such as, for example, the same broad product grouping but different customers that are managed differently by the bank; |

| (gg) |

reference data that include accrued interest, other due payments and limit excesses, that is, the bank’s EAD reference data shall not, for example, be capped to the principal amount outstanding or any facility limit; |

| (hh) |

appropriate homogenous segments, that is, the bank shall ensure that its EAD estimates are not, for example, essentially based upon, or partly based upon: |

| (i) |

SME/midmarket data being applied to large corporate borrowers or obligors; |

| (ii) |

Data from commitments with substantially low unused limit availability being applied to facilities with substantially large unused limit availability; |

| (iii) |

Data from borrowers or obligors identified as problematic at reference date, such as, for example, customers who are delinquent, watch listed by the bank, subject to bank-initiated limit reductions, blocked from further drawdowns or subject to other types of collections activity, being applied to borrowers or obligors that are fully current with no known problems; |

| (iv) |

Data affected by changes in obligors’ mix of borrowing and other credit-related products over the observation period; |

| (ii) |

an estimation technique that performs well in out-of-sample tests; |

| (vi) |

shall appropriately take into consideration all relevant and material information; |

| (vii) |

shall be based upon the definition of default, specified in regulation 67; |

| (viii) |

may take into account data from external sources, including pooled data, provided that— |

| (aa) |

the EAD estimates shall represent long-run experience; |

| (bb) |

when the bank bases its estimates on alternative measures of central tendency, such as, for example, the median or a higher percentile estimate, or only on ‘downturn’ data, the bank shall ensure that its estimates do not fall below a conservative estimate of the relevant long-run default-weighted average EAD for similar eligible facilities; |

| (ix) |

shall be based upon historical experience and empirical evidence; |

| (x) |

shall be reviewed on a regular basis, but not less frequently than once a year, or when material new information is obtained; |

| (xi) |

shall be based upon comprehensive policies, systems and procedures, which shall be adequate— |

| (aa) |

to prevent further drawings in circumstances short of payment default, such as covenant violations or other technical default events; |

| (bb) |

to monitor, on a daily basis, facility amounts and current outstanding amounts against committed lines; |

| (cc) |

to monitor any changes in outstanding amounts per borrower, and per risk grade; |

[Regulation 23(13)(b)(v)(D) substituted by section 2(rrrrrr) of Notice 6342, GG52907, dated 26 June 2025, shall come into operation on 1 July 2025]

| (E) |

shall in the case of exposures to corporate institutions, sovereigns or banks calculate the effective maturity in respect of each relevant exposure, which effective maturity shall be calculated in accordance with and comply with the relevant minimum requirements specified in paragraph (d)(ii)(B) below. |

| (vi) |

Validation of internal estimates |

As a minimum, a bank that adopted the advanced IRB approach for the measurement of the bank's exposure to credit risk—

| (A) |

shall comply with the relevant requirements specified in subregulation (11)(b)(x) above and such further conditions as may be specified in writing by the Registrar; |

| (B) |

shall for each relevant risk grade regularly compare realised PD ratios, LGD ratios and EAD amounts with estimated PD ratios, LGD ratios and EAD amounts, and demonstrate to the satisfaction of the Registrar that the realised risk components are within the expected range of risk components for a particular grade; |

| (C) |

shall duly document the data and methods used to compare realised default rates, LGD ratios and EAD amounts with estimated PD ratios, LGD ratios and EAD amounts in respect of each relevant risk grade, including the periods that were covered and any changes in the data and methods that were used, which analysis and documentation shall be updated at appropriate intervals but not less frequently than once every year; |

| (D) |

shall have in place sufficiently robust internal standards to deal with situations where realised PD ratios, LGD ratios and EAD amounts substantially deviate from expected PD ratios, LGD ratios and EAD amounts provided that when the realised values continue to be higher than the expected values, the bank shall adjust its estimates of risk components upward in order to reflect the appropriate default and loss experiences of the bank. |

Superior Courts Act, 2013

Superior Courts Act, 2013