National Nuclear Regulator Act, 1999

National Nuclear Regulator Act, 1999

R 385

Public Finance Management Act, 1999 (Act No. 1 of 1999)Understanding and Using this ActNational Treasury Guidelines for Annual Reporting2. Background |

| 1) | When a government is voted into office, an inevitable contract of accountability is entered into between government and the citizens it serves. It is therefore incumbent on government to inform the citizens on what they intend to achieve against pre-determined objectives. These pre-determined objectives are reflected in the strategic plans and the annual budgets of departments. Published strategic plans make government operations transparent to the legislatures and are key instruments in the accountability and budgeting process. These strategic plans also provide essential information for the legislatures to assess proposed programmes and funding. They also enable the legislatures to evaluate departmental performance when performance measures and indicators are published in annual reports. |

| 2) | Strategic planning cannot be developed in isolation but should rather be the result of thorough consultation with all relevant stakeholders. The following must be aligned to and be consistent with the strategic plan: |

| a) | estimates of expenditure; |

| b) | performance contracts between a Minister/MEC and the head of the department; |

| c) | performance contracts between the head of a department and senior managers; |

| d) | service delivery improvement programme; and |

| e) | departmental annual reports. |

| 3) | From the aforegoing, it is evident that the accountability process culminates with the publishing of the annual report, which serves to inform the citizens of the country as to what progress Government has made in the achievement of its objectives. Accounting officers are therefore required to compile annual reports for the institutions that they are responsible for and these annual reports must fairly represent their institution’s performance and financial position for a particular fiscal year. The information contained in the annual report should reflect the institution’s achievements in relation to the objectives as set out in year 1 of the institution’s strategic plan and annual budget for the fiscal year in question. |

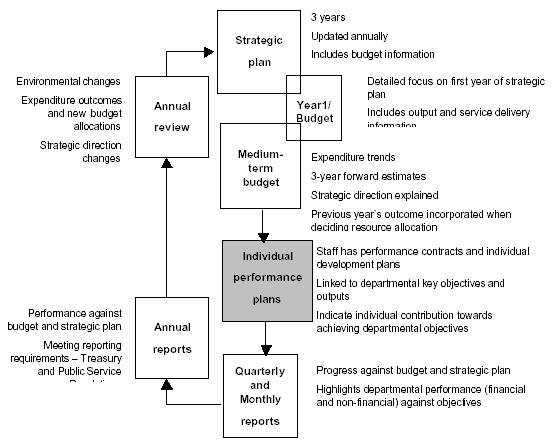

| 4) | The following is a diagrammatic representation of the planning, budgeting and reporting cycle: |

Planning, budgeting and reporting cycle

| 5) | The executive authority must critically assess this annual report, which must be presented to Parliament or the relevant provincial legislature. |