Businesses Act, 1991 (Act No. 71 of 1991)

Businesses Act, 1991 (Act No. 71 of 1991)

R 385

Auditing Profession Act, 2005 (Act No. 26 of 2005)NoticesRegulatory Strategy for Independent Regulatory Board for AuditorsPart A : General InformationOverview of the IRBA |

The IRBA is the statutory body controlling the auditing profession in South Africa. The general functions ascribed to it, in terms of the APA, are as follows:

| “4. |

| (1) | The Regulatory Board must, in addition to its other functions provided for in this Act: |

| (a) | Take steps to promote the integrity of the auditing profession, including: |

| (i) | investigating alleged improper conduct; |

| (ii) | conducting disciplinary hearings; |

| (iii) | imposing sanctions for improper conduct; and |

| (iv) | conducting practice reviews or inspections; |

| (b) | Take steps it considers necessary to protect the public in their dealings with registered auditors; |

| (c) | Prescribe standards of professional competence, ethics and conduct of registered auditors; |

| (d) | Encourage education in connection with, and research into, any matter affecting the auditing profession; and |

| (e) | Prescribe auditing standards. |

| (2) | The Regulatory Board may: |

| (a) | Participate in the activities of international bodies whose main purpose is to develop and set auditing standards and to promote the auditing profession; |

| (b) | Publish a journal or any other publication, and issue newsletters and circulars containing information and guidelines relating to the auditing profession; |

| (c) | Cooperate with international regulators in respect of matters relating to audits and auditors; and |

| (d) | Take any measures it considers necessary for the proper performance and exercise of its functions or duties or to achieve the objects of this Act.” |

The IRBA Strategic Focus

Our strategic focus is to protect the financial and non-financial interests of the public by ensuring that only suitably qualified individuals are admitted to the auditing profession, and that registered auditors deliver services of the highest quality and adhere to the highest ethics standards.

The IRBA Vision

To be a preeminent, internationally respected and locally recognised audit regulator, whose purpose is to protect the public interest and safeguard the integrity of the South African financial markets by creating an enabling environment in which auditors can deliver high-quality audits.

The IRBA Mission

We endeavour to protect the financial interests of the investing community by creating and enhancing regulatory tools and principles, to empower registered auditors to carry out their duties competently, independently and in good faith.

The IRBA Objectives

In line with our legislative mandate, the IRBA’s objectives are to:

| • | Build credibility for the IRBA, as a proactive regulator of the auditing profession. |

| • | Demonstrate relevance and responsiveness (to changes/market expectations) by initiating improvements in the auditing profession. |

| • | Increase audit firm transparency. |

| • | Align auditor behaviour and integrity with ethical requirements. |

| • | Align auditor skills to the Competency Framework. |

| • | Improve the quality of audits and address investor expectations. |

| • | Manage the public’s (private and public sectors) expectations of the auditor’s role. |

| • | Promote stability and growth in capital markets. |

The IRBA Goal

Our goal is to be seen as an effective and impactful regulator that can change the behaviour of auditors and influence other roleplayers in the financial reporting system to:

| • | Improve audit quality; |

| • | Improve ethics and independence; and |

| • | Improve the transparency of audit firm practices. |

Regulatory Philosophy

The IRBA’s regulation is focused on the protection of the public’s financial and non-financial interests, while it recognises its role in creating an enabling environment in which auditors can deliver high-quality audits.

Value Proposition

The IRBA creates continuing value through its role as an embedded protector of confidence in the sustainability of the financial reporting system, while creating an enabling environment for auditors who practise the auditing profession in good faith, thereby contributing to the protection of the public’s financial and non-financial interests.

The IRBA Values

As the overall custodian of the auditing profession in South Africa, the IRBA acknowledges the importance of the mandate assigned to it by Parliament, and all its registrants and employees ascribe to the following core values:

Independence, Integrity and Objectivity

It is imperative that we are not just independent of the auditing profession in our composition and membership, but also reflect independence in the perception of our key stakeholders through our actions and behaviour. Therefore, it is important that we act with integrity and objectivity in our deliberations, decisions and actions.

Commitment to Public Interest

We recognise the scope and extent of our mandate in respect of both the public and the profession and undertake to execute and deliver on this mandate with diligence and commitment in terms of our vision.

Transparency and Accountability

As a public entity in the overall delivery structure of the South African government, and a beneficiary of public funds, we promote transparency in our interactions with the relevant stakeholders and recognise our accountability to the Parliament of South Africa and the Minister of Finance as our Executive Authority.

Legislative Mandate

As noted in the Foreword, the IRBA was established in terms of section 3 of the APA, and the objects of the Act are clearly set out in section 2.

Our Key Priorities and Strategic Outcomes

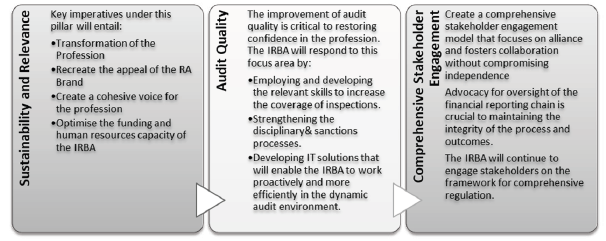

The IRBA is committed to enhancing audit quality and addressing gaps in the auditing profession and the broader financial reporting and governance ecosystem, with a specific focus on three areas that affect audit quality, and thereby ensuring the continued sustainability and relevance of both the IRBA as a regulator and the profession.

The focus areas are expanded in more detail in Part B: IRBA Mandate.

Guiding Principles When We Perform Our Regulatory and Operational Activities

The IRBA has committed itself to the following relevant guiding principles:

| • | Ensuring that it is effective, transparent and accountable. |

| • | Respecting the constitutional status, powers and functions of organs of State, statutory or regulatory bodies. |

| • | Exercising its powers and performing its functions in a manner that does not encroach on the geographical, functional or institutional integrity of organs of State, statutory or regulatory bodies. |

| • | Co-operating with organs of State, statutory or regulatory bodies in mutual trust and good faith by fostering friendly relations and assisting and supporting these, as allowed within the limitations of the APA. |

| • | Informing other regulators, institutions and government entities of, and consulting with them on, matters of common interest. |

| • | Co-ordinating its actions and regulatory actions with other relevant persons or bodies. |

| • | Adhering to the relevant provisions of the Public Finance Management Act 1999 (Act No. 1 of 1999) (PFMA). |

| • | Ensuring that in the procurement of goods or services, it does so in accordance with a system that is fair, equitable, transparent, competitive and cost-effective. |

Our Engagement with Stakeholders as We Implement Our Regulatory Strategy

We recognise that we have a statutory obligation to drive and influence broader systemic change and reforms within the profession.

However, for our strategic review to be encompassing and meet the legislative mandate of the IRBA, we need to engage more broadly with relevant stakeholders and seek their participation in the review process.

As such, through our targeted engagements we will continue to collaborate with our stakeholders, who have expressed a need for a more collaborative regulator that will enable the formation of a cohesive voice for the profession to restore trust and confidence, while maintaining our regulatory independence.